language

At this seminar, our trust and financial advisors explained how to integrate insurance and trust structures to identify potential risks in using insurance as a wealth transfer tool — and how to address them through strategic planning.

Insurance remains one of the most common wealth transfer tools in Taiwan. It provides quick payouts, allows designation of beneficiaries, and helps cover immediate liquidity needs such as end-of-life expenses, estate taxes, or outstanding loans.

However, when viewed within a comprehensive succession framework, insurance alone is not a complete solution. Significant gaps remain in taxation, creditor protection, and cross-border compliance — all of which require structural design to resolve.

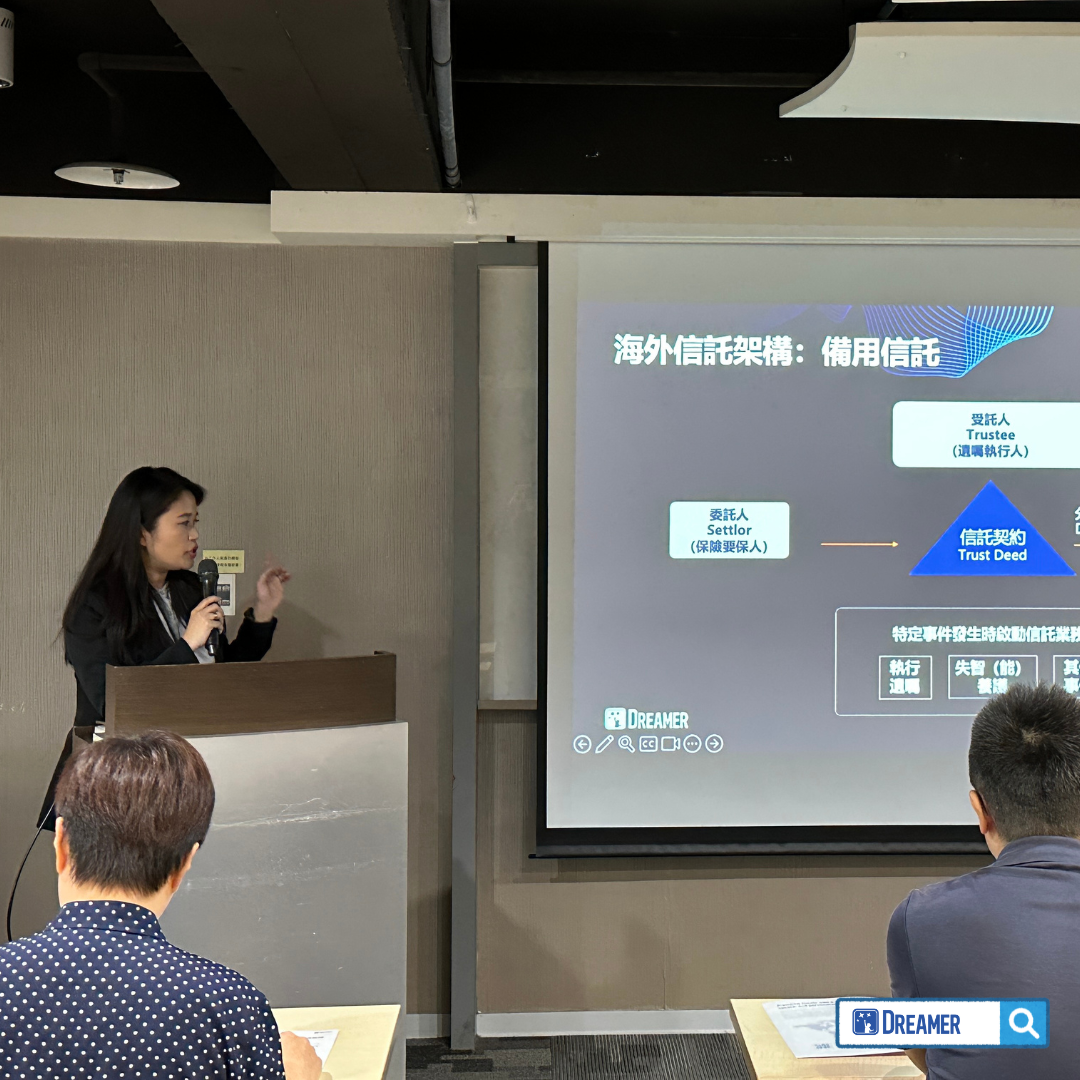

By combining insurance with a trust structure, policy proceeds can be distributed conditionally, periodically, or at specific times in accordance with the policyholder’s intent. This ensures the funds reach the intended family members while reducing exposure to beneficiary debts, legal disputes, or asset risks.

Jolene shared the unique advantages of Universal Life (UL) insurance and clarified two commonly misunderstood financial concepts — Policy Loans and Premium Financing — which, while often confused, are fundamentally different.

- Policy Loan:

A policy loan is a loan from the insurance company, using the policy’s cash value as collateral. Interest accrues as agreed and, if unpaid, is deducted from the surrender value or death benefit. This method is simple and suitable for short-term liquidity, but if left unpaid for too long, compounding interest may erode the policy’s value or even cause it to lapse.

- Premium Financing:

In contrast, premium financing involves borrowing from a bank or financial institution to pay high-value premiums. The policy is typically pledged as collateral, sometimes along with additional assets. Most loans are interest-only, with the principal repaid later through cash flow, asset liquidation, partial policy surrender, or the final death benefit.

In recent years, premium financing has become increasingly popular among high-net-worth individuals due to three key advantages — efficiency, leverage, and governance.

1. Capital Efficiency:

By using external financing to pay premiums, personal capital can remain invested in higher-return, more liquid assets such as core businesses, private equity, or real estate.

2. Leverage Effect:

Life insurance inherently carries time value through long-term cash flows and death benefits. Leveraging financing allows policyholders to achieve greater coverage and liquidity with less personal capital — for example, preparing funds for future estate taxes, structuring unequal but controlled distributions, or integrating with family holdings, ESOPs, or charitable trusts to build a long-term “cash engine.”

3. Governance Impact:

Premium-financed policies are often held within trusts, embedding rules for beneficiary conditions, payout schedules, collateral management, and refinancing. This allows financial flows to align with family governance structures, ensuring flexibility and oversight.

The information provided on this website is for general information purposes only and does not constitute an offer, and the Website and all information provided to you via the website are provided “as is” and “as available”, the content described herein is subject to change without notice from Dreamer Group Limited and/or any of its members, affiliated entities (Dreamer Group Limited and all its members and affiliated entities collectively referred to as the “Dreamer Group” herein after). We will strive to ensure the integrity and accuracy of the website's functionality and content, while, to the maximum extent permitted by applicable law, we disclaim all express, implied, and statutory warranties with respect to the same, including without limitation any implied warranties of merchantability, satisfactory quality, fitness for a particular purpose, accuracy, completeness, non-infringement, non-interference, error-free service, and uninterrupted service.

By making available the websites, Dreamer Group is not making an offer of any financial, tax, accounting, legal or other professional services or goods, and none of the information presented on the websites should be construed as finance, tax, accounting, legal or any other professional advice or service. You should always seek the advice of a suitably qualified professional before taking or refraining from taking any action. Dreamer Group will not be liable in any way to any person for any action taken or omitted to be taken as a result of the use of any content posted by us, which results in, causes or gives rise to any loss.

The laws of some jurisdictions may impose restrictions on the distribution of materials described on this Site. This Site is not directed to persons in jurisdictions where such restrictions apply. If you belong to such areas or you are in such areas, please exit this website immediately and you will be responsible for any losses, controversies, disputes and other negative consequences arising from your continued browsing.

All information, text and images on this website are copyrighted or registered by DREAMER GROUP.

We urge all persons contacting Dreamer Group to check the website and service number carefully and to remain vigilant to avoid being deceived or misled by unscrupulous persons.

This disclaimer is written in Chinese and the English version is provided for information purposes only.